Economic Snapshot

March 2025

Summary

March was marked by heightened uncertainty surrounding President Trump’s tariff threats, significantly weakening investor sentiment. Concerns over a potential economic slowdown and the inflationary effects of tariffs drove fears, culminating in sharp global equity market selloffs with investors shifting to more defensive positioning.

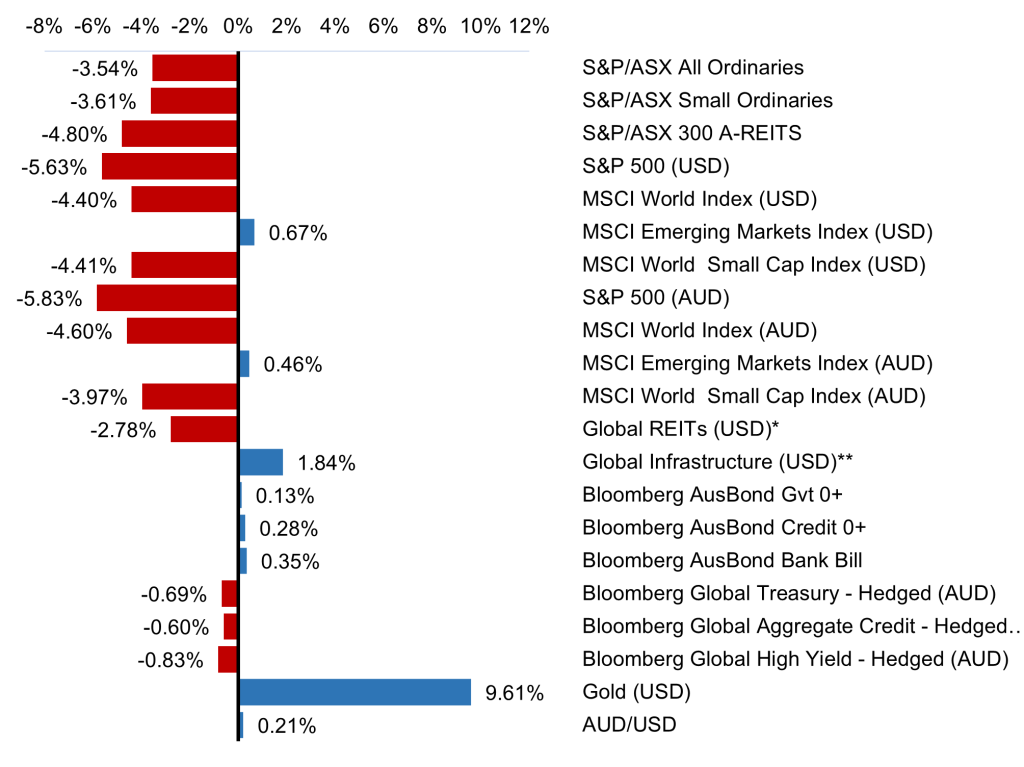

Selected market returns (%), March 2025

Sources: *FTSE EPRA/NAREIT DEVELOPED, **FTSE Global Core Infrastructure 50/50 Index

Key market and economic developments in March 2025

Financial markets

Global equities continued to decline in March, with the MSCI World Index (USD) down 4.4%. Volatility increased, reflecting heightened uncertainties about the potential negative economic impacts of US trade and economic policies. Developed markets saw broad selloffs, while Chinese and Indian equities helped lift emerging markets. Bond yields remained largely stable.

Australian equities

The S&P/ASX All Ordinaries fell 3.5%, moving into negative territory for the year-to-date. Weakness persisted across sectors, with the MidCap 50 and Small Ordinaries indices declining 3.5% and 3.6%, respectively. Utilities gained 1.5% as investors sought defensive assets. Despite solid gains in industrial and precious metals, a 24% drop in the shares of James Hardie Industries, on the back of a significant acquisition announcement, weighed on the Materials sector, which closed 0.3% lower. Information Technology led declines for the second month, ending 9.7% lower, followed by the Consumer Discretionary sector, which fell 6.3%.

Global equities

US equities led developed market declines, with the S&P 500 (USD) down 5.6% to a six-month low. The Nasdaq (USD) posted a 7.7% drop, its worst quarter in nearly three years, as several mega cap technology stocks posted double-digit declines. Investor positioning continued to move away from US exposures in what has been a consensus overweight position in recent years. The Russell 2000 Index (USD) fell 7%, weakening further, as the economically sensitive sector’s performance was impacted by a more uncertain US economic outlook.

European equities also struggled, with the Euro 100 (EUR) declining by 1.9%. Nevertheless, the region concluded the first quarter with strong gains, largely driven by German large-cap stocks that were buoyed by expectations of increased government spending. The Hang Seng (HKD) rose by 0.8%, benefiting from positive investor sentiment following Chinese authorities’ pledges of economic stimulus. Indian equities rallied, with the Nifty 50 (INR) climbing 6.3%, recovering from oversold levels.

Commodities

Gold surged 9.6% to close at US$3122/oz, as investors sought a safe haven amid trade and geopolitical uncertainty. Precious metals, including silver and platinum, were also significantly higher, supported by a weaker US dollar. The copper price continued to rise, gaining 12.4%, supported by both Chinese stimulus and the threat of US tariffs on copper imports. Brent crude oil held steady at $72.35 per barrel.

Bond markets

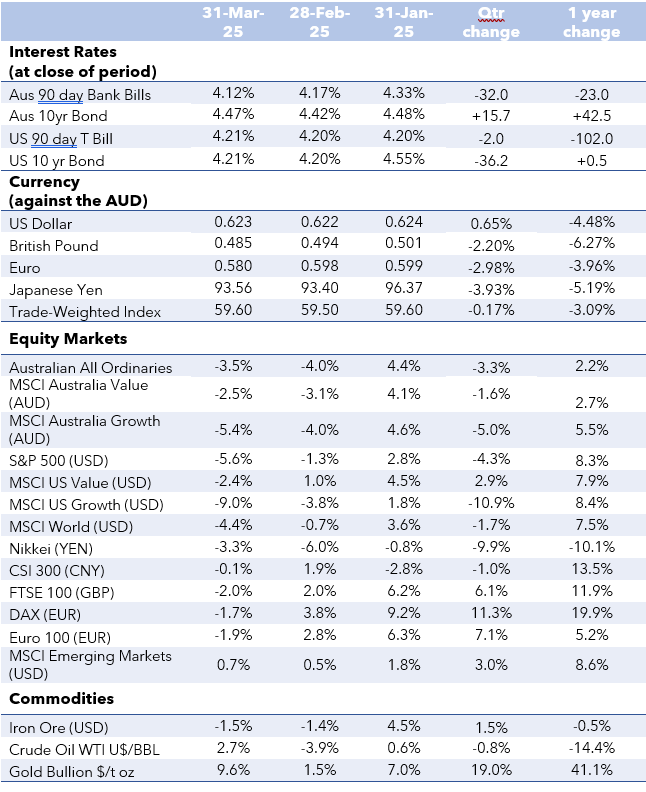

Bond markets traded sideways in both the US and Australia. The Australian 10-year yield rose 5 basis points to 4.47% despite lower-than-expected domestic inflation. The US 10-year yield remained stable at 4.21% as the inflationary impacts of tariffs were weighed against a potential slowdown in US economic activity. Germany experienced a major bond selloff, with its 10-year yield surging 31 basis points in one day, the sharpest move since 1997, following a significant increase in government spending plans.

Economic developments

Australian growth improves with inflation continuing to moderate

Q4 GDP showed some improvement, rising slightly more than expected to 1.3% year-on-year, up from 0.8%. The underlying data highlighted stronger private consumer spending aided by income tax cuts, but productivity remained poor with GDP per hour worked falling by 1.2% over the year.

Consumer confidence rose 4% to a three-year high as consumers responded favourably to the Reserve Bank of Australia’s (RBA) mid-February interest rate cut. Consumers’ expectations of unemployment remained very low. The unemployment rate was unchanged at 4.1%, but employment numbers showed a surprising fall of 53,000, impacted by fewer older workers returning to the jobs market.

Monthly headline CPI rose 2.4% year-on-year, lower than the 2.5% economists had expected. In a positive signal for the interest rate outlook, stickier subcomponents of the CPI basket such as rent, insurance and new housing costs continued to show slower price increases.

Uncertainty clouds the US economic outlook while Germany lifts fiscal spending

The Trump administration’s volatile trade policy continued to raise levels of economic uncertainty. This negatively impacted “soft” economic data releases across both business and consumer surveys of current conditions and future expectations, where worries of rising inflation and slower growth hampered sentiment and activity levels.

The US Federal Reserve (Fed) held rates steady as expected. Chair Powell’s comments in the press conference highlighted the increased levels of uncertainty related to fiscal and trade policies and their subsequent impacts on both growth and inflation. The Fed revised their 2025 economic growth from 2.1% to 1.7% while revising the PCE inflation forecast higher from 2.5% to 2.8%. Expectations from the median Federal Open Market Committee (FOMC) are for two interest rate cuts this year.

Germany signalled a significant shift from a conservative fiscal stance where the government announced a €500 billion infrastructure investment fund alongside reforms to its “debt brake” rule, which traditionally capped borrowing. These changes are expected to allow for increased fiscal flexibility to address economic stagnation and geopolitical challenges.

Chinese authorities maintained their 5% GDP growth target for 2025 while also announcing a planned increase in the budget deficit from 3% to 4% of GDP, the largest in more than three decades. Additional stimulus measures were also announced to further boost the Chinese economy.

Outlook

The increasing risk of a global trade war has heightened investor fears of a US recession, leading to a repricing of global financial markets to reflect higher risk premiums. Although consensus forecasts still predict that the US will avoid a recession this year, persistent economic uncertainty could impede growth. However, a de-escalation of trade tensions and clearer trade policies could lead to market stabilisation and a potential recovery in risk assets after a significant derating.

In an environment where unsettling headlines often dominate the narrative, investors should not overlook the positive factors that can inform strategic decision-making. Successfully navigating this environment requires a disciplined yet dynamic approach to portfolio management.

Major market indicators

Sources: Quilla, Refinitiv Datastream