Economic Snapshot

February 2026

Summary

The rotation away from the United States (US) technology exposure continued in February, with most other major markets outperforming. Korean and Japanese equities led the charge, supported by better-than-expected economic data and continued earnings growth, which is a tailwind for international returns broadly.

Within the United States, the Supreme Court’s ruling striking down emergency tariff powers was negated when the Trump administration signalled that alternative mechanisms would be used. Energy, materials, and industrials continued to attract flows away from mega-cap technology, with the Artificial Intelligence (AI) thematic remaining in a period of earnings validation. Nvidia’s results beat expectations, but the stock fell, reflecting a more cautious investor posture towards AI and the broader technology sector.

Australian equities had a strong month, led by banks, materials and energy. Though the RBA’s rate hike to 3.85% introduced intra-month volatility for rate-sensitive financials and real estate names.

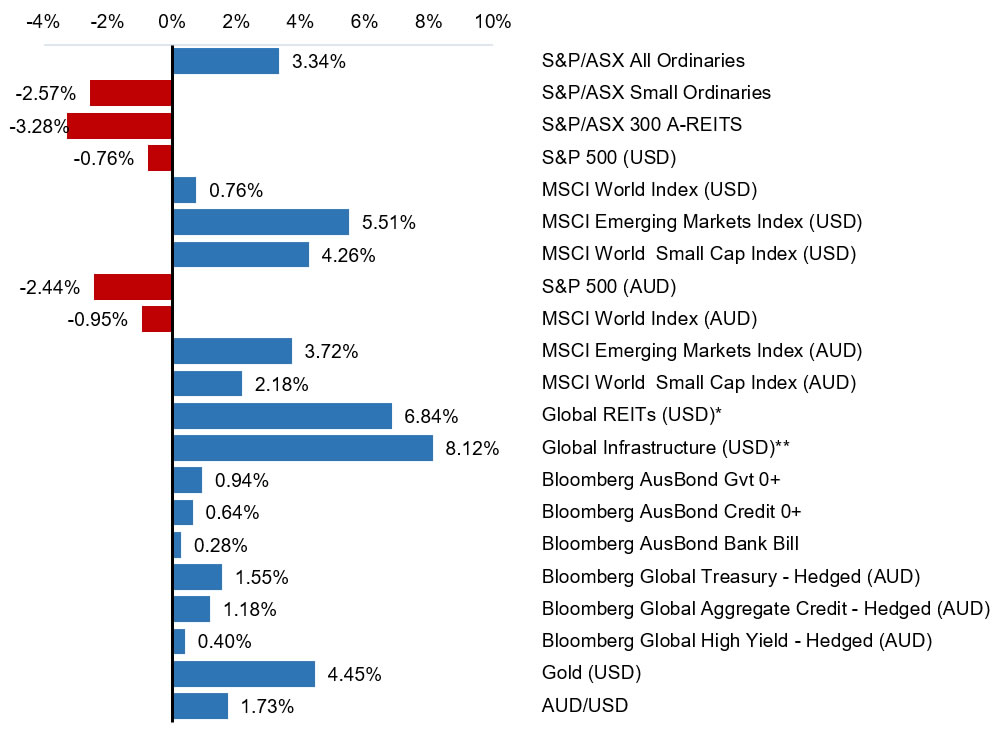

Selected Market Returns (%)

FEBRUARY 2026

Sources: *FTSE EPRA/NAREIT DEVELOPED, **FTSE Global Core Infrastructure 50/50 Index

Financial markets

Global equity markets were mixed in February, posting modest gains, with the MSCI World Index (USD) up 0.76%. The AI thematic remained a key driver of volatility, as the market continued to favour hardware and infrastructure over software names amid concerns regarding the

monetisation of AI. Australian equities outperformed in February, with the reporting season delivering strong results across the major banks and the materials sector. US bond yields declined on the back of softer retail and GDP data, alongside safe-haven demand stemming from tariff-driven market uncertainty.

Australian equities

The S&P/ASX All Ordinaries Index gained 3.34% in February, driven by a strong domestic reporting season and selective strength in commodities. The RBA’s decision to raise the cash rate to 3.85% introduced volatility for rate-sensitive sectors, though this was offset by broad earnings momentum across the market.

The financials sector was a standout contributor to the index. The major banks delivered a resounding beat across key metrics, including revenue, net interest margins, costs, dividends, and credit quality.

The resources sector also contributed positively. Materials stocks were supported by firm copper prices and a positive reporting season for major miners, with BHP reaching record highs following a strong half-year earnings result. Gold producers contributed as the gold price remained near historic highs set in January. In contrast, Iron ore faced headwinds, with prices softening amid subdued Chinese demand.

Rate-sensitive market segments faced headwinds. Real estate stocks came under pressure as bond yields moved higher and the RBA’s rate hike reinforced expectations of a prolonged tightening cycle. Technology and growth names also struggled, with concerns around AI disruption.

The S&P/ASX Small Ordinaries Index returned -2.57% for the month, with losses broad-based across the index after the RBA hiked rates.

Global equities

Global equity markets’ performance was mixed in February, with most major indices outperforming the US as the rotation away from mega-cap technology continued.

European and Japanese equities both extended their recent runs, supported by better-than-expected economic data, fiscal stimulus momentum, and strong corporate earnings. In Japan, political clarity under PM Takaichi and expectations of continued fiscal expansion were additional tailwinds.

The AI thematic remained a source of uncertainty, with Nvidia’s post-earnings retreat reflecting broader investor caution around the pace of earnings uplift from AI investment.

Value-oriented and cyclical sectors continued to attract flows at the expense of long-duration growth names. The S&P 500 returned -0.76% (USD), weighed down by the Software and Services sector, where AI disruption fears caused further angst. The small-cap Russell 2000, in contrast, returned 0.71% (USD), and emerging markets returned 5.51% (USD), the latter supported by AI supply chain strength across Asia.

Commodities

Gold rebounded after a sharp sell-off at the start of February, trading above $5,270 per ounce by month’s end and gaining approximately 4.45% (USD). Silver gained 25.86% (USD), supported by increased retail investor participation, while copper remained stable on electrification and AI infrastructure themes.

West Texas Intermediate crude oil gained 3.8% (USD), reaching a six-month high as escalating US-Iran tensions drove a meaningful risk premium into energy markets.

Bond markets

US and Australian bond markets followed divergent paths in February, reflecting markedly different domestic monetary policy outlooks.

US Treasury yields declined in February as softer spending and activity data raised questions about growth momentum, while renewed tariff-related volatility and safe-haven flows added further support to bonds. The 10-year Treasury yield fell approximately 25 basis points over the month to close at 3.96%.

In Australia, the RBA’s rate hike set a hawkish tone from the outset. Robust employment data and persistent inflation, with headline CPI holding at 3.8% and trimmed mean inflation edging higher, reinforced expectations of further tightening. The Australian 10-year yield closed at approximately 4.65% for the month.

Economic developments

The tariff merry-go-round

The tariff landscape shifted in February, with the Supreme Court ruling that the President’s use of emergency powers to impose reciprocal tariffs was unlawful. The decision initially triggered a sharp risk-on move across equity and currency markets before the administration moved quickly to reimpose levies through an alternative legislative mechanism.

The episode highlighted the degree to which trade policy uncertainty has become a structural feature of the current market environment rather than a transitory concern. While the legal challenge created a brief window of relief, the net outcome left the global trade landscape largely unchanged, and the prospect of further escalation remains. Retaliatory measures from key trading partners, including the European Union and China, continue to be flagged, and the situation remains fluid.

The hike nobody wanted

The RBA’s decision to raise the official cash rate by 25 basis points to 3.85% at its February meeting was a defining moment for monetary policy. The move was the first hike in over two years. The decision reflected the Board’s concern that inflation, having appeared to be on a downward path, has proven more persistent than anticipated.

The data underpinning the decision was difficult to look past. Headline CPI rose to 3.8% in the December quarter, well above the RBA’s 2 to 3% target band, with services inflation and housing costs remaining the most stubborn contributors. Wage growth also came in above expectations for the fourth quarter, reinforcing the view that domestic cost pressures have not yet sufficiently abated. Following the decision, markets moved quickly to price a high probability of a further hike at the May meeting, with the peak in the cash rate now expected to be meaningfully higher than was anticipated late last year.

Outlook

Global economic growth is expected to remain positive, though ongoing geopolitical risks and trade policy uncertainty have introduced a more cautious tone. Resilient labour markets, continued fiscal support, and solid corporate earnings provide an offsetting foundation for risk assets, but the tariff environment remains a significant source of uncertainty.

The AI thematic continues to present a compelling medium-term opportunity, though the market’s response to Nvidia’s February earnings illustrated a meaningful shift in investor focus. The debate has moved beyond near-term earnings delivery and toward questions of monetisation, return on capital, and the durability of hyperscaler spending. The outlook remains constructive where AI investment is beginning to translate into measurable commercial outcomes, but broader sector performance is likely to remain uneven until that earnings uplift becomes more visible across the broader market and sub-sectors within technology, such as software.

Domestically, the RBA’s return to a hiking cycle represents a meaningful shift in the Australian economic backdrop. Rate-sensitive sectors face a more challenging near-term environment, while the resources sector continues to offer some insulation from structural commodity demand and elevated gold prices.

Near-term conditions are likely to remain volatile as investors navigate diverging central bank trajectories, evolving trade policy, rising geopolitical uncertainty, and the ongoing validation of the AI earnings cycle. Portfolio diversification and a focus on earnings quality remain important disciplines in this environment.

Major market indicators

| 28-Feb-26 | 31-Jan-26 | 31-Dec-25 | Qtr change | 1 year change | |

| Interest Rates (at close of period) | |||||

| Aus 90-day Bank Bills | 3.96% | 3.77% | 3.71% | +31.0 | -21.0 |

| Aus 10yr Bond | 4.65% | 4.75% | 4.72% | +23.4 | +22.7 |

| US 90-day T-Bill | 3.59% | 3.58% | 3.57% | -14.0 | -61.0 |

| US 10 yr Bond | 3.96% | 4.26% | 4.16% | -5.5 | -23.3 |

| Currency (against the AUD) | |||||

| US Dollar | 0.713 | 0.701 | 0.667 | 8.67% | 14.60% |

| British Pound | 0.528 | 0.509 | 0.497 | 6.99% | 6.93% |

| Euro | 0.603 | 0.587 | 0.570 | 7.01% | 0.85% |

| Japanese Yen | 111.15 | 107.77 | 104.53 | 8.67% | 19.00% |

| Trade-Weighted Index | 65.50 | 64.50 | 62.20 | 7.03% | 10.08% |

| Equity Markets | |||||

| Australian All Ordinaries | 3.3% | 1.6% | 1.3% | 6.3% | 15.8% |

| MSCI Australia Value (AUD) | 7.6% | 2.6% | 2.7% | 13.4% | 24.3% |

| MSCI Australia Growth (AUD) | 0.8% | -0.4% | -0.9% | -0.5% | -4.3% |

| S&P 500 (USD) | -0.8% | 1.5% | 0.1% | 0.7% | 17.0% |

| MSCI US Value (USD) | 1.8% | 4.5% | 0.8% | 7.2% | 14.7% |

| MSCI US Growth (USD) | -3.8% | -1.9% | -0.7% | -6.3% | 16.7% |

| MSCI World (USD) | 0.8% | 2.3% | 0.8% | 3.9% | 21.8% |

| Nikkei (YEN) | 10.4% | 5.9% | 0.3% | 17.3% | 61.5% |

| CSI 300 (CNY) | 0.2% | 1.8% | 2.5% | 4.5% | 24.5% |

| FTSE 100 (GBP) | 7.0% | 3.0% | 2.3% | 12.7% | 28.1% |

| DAX (EUR) | 3.0% | 0.2% | 2.7% | 6.1% | 12.1% |

| Euro 100 (EUR) | 4.2% | 3.0% | 1.1% | 8.5% | 20.5% |

| MSCI Emerging Markets (USD) | 5.5% | 8.9% | 3.0% | 18.3% | 50.8% |

| Commodities | |||||

| Iron Ore (USD) | -5.2% | -2.6% | 1.9% | -7.8% | -4.9% |

| Crude Oil WTI U$/BBL | 3.8% | 12.6% | -2.3% | 16.9% | -4.3% |

| Gold Bullion $/t oz | 4.4% | 16.3% | 3.0% | 21.5% | 84.3% |

Sources: Quilla, Refinitiv Datastream